It shouldn’t really be a surprise, but dignity at work – a combination of things such as the sense of autonomy and relationships with colleagues and bosses, and being treated fairly – matters to people. It’s as true at the bottom of the income scale, where observers might assume concerns about pay outweigh all other considerations, as it is higher up. Dignity matters to people, as I’ve been exploring in recent blogs.

For the book I am writing (on fairness in business and investment) I am currently investigating the literature on monopsony and oligopsony in labour markets. Monopsony is the distorted market situation arising from there being a single buyer of a good or service (a monopoly is where there’s a single seller); oligopsony is where there is a narrow enough group of buyers that they distort the marketplace. Economists are increasingly observing evidence that the labour market suffers inefficiencies that are consistent with oligopsony – employers having excess power in setting pay. Most workers would probably agree that their experiences too are consistent with this.

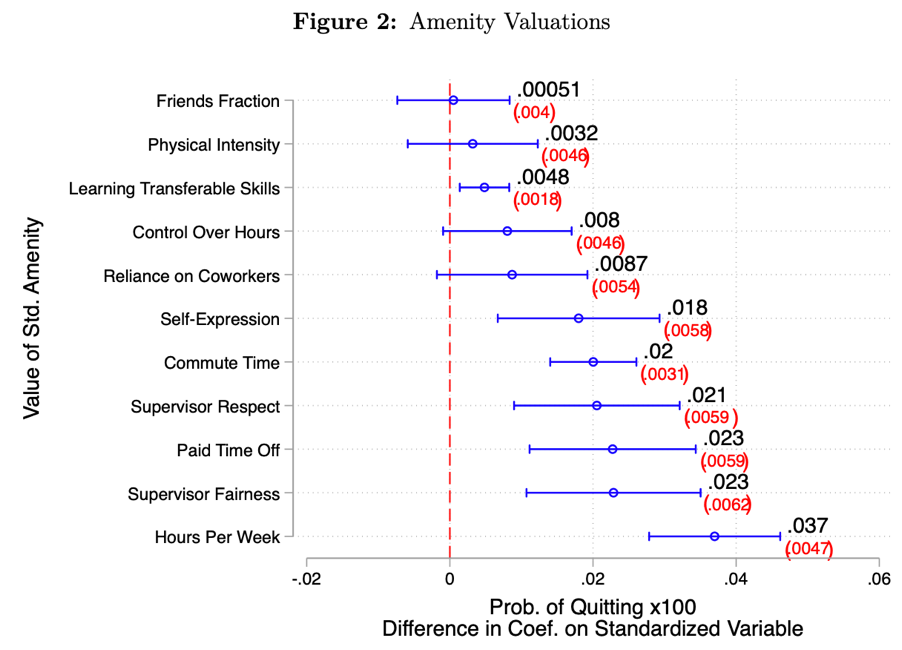

The study included four sentences exploring the degree to which workers had a sense of dignity in their jobs (these sentences were developed based on prior interviews with Wal-Mart workers that sought to understand their experience in the workplace, as well as earlier academic work). The overarching question was Indicate to what extent the sentence describes the workplace of your job at Walmart, and each time respondents were offered four responses (Almost Always; Often; Sometimes; Never). The four sentences were:

You [have/had] the opportunity to express yourself while at work.

You [can/could] rely on your co-workers to help you with work.

Your supervisor [treats/treated] you with respect.

Your supervisor [treats/treated] everyone fairly.

And of these four measures of dignity, it appears to be fairness that matters most. Indeed, a lack of fair treatment by one’s boss is in essence the greatest determinant of likelihood of quitting a job in the study, with the obvious exception of pay (and of the availability of hours of work a week, which is a clear part of the pay equation for those paid on an hourly basis):

Consistently, the study confirms that fairness and dignity are powerful drivers of work satisfaction, and thus in willingness to stay with an employer.

As the study states:

“A natural question is whether firms can adjust the level of dignity at work. While immediate supervisors likely have the most discretion over workplace dignity, supervisors can be incentivized by higher-level managers to treat subordinates fairly and with respect, and workplace rules can be designed to allow opportunities for self-expression and co-worker support. While it may take time to alter workplace experiences, and agency costs might be considerable, the significant cross-store variation we document below suggests that managers have some control over the level of workplace dignity.”

Our bosses, and how they treat us, matter.

As well as enhancing people management, the authors raise the interesting challenge of whether improving the competitive context of the labour market is necessary to increase dignity in the workplace, the experience of fairness for workers:

“any effort to increase workplace amenities (including subjective experiences at low-wage jobs) may require policies that reduce monopsony power in the low-wage labor market. The high levels of labor market competition in the immediate post-COVID labor market may have given workers the opportunity to quit jobs that didn’t provide dignity. Whether this results in firms upgrading the subjective experience of work remains to be seen.”

I’m not sure that we’ve yet seen significant enhancements to workplace dignity and fairness, but perhaps we should continue to live in hope.

The modern mind profoundly misunderstands our ancient ancestors. Take the mystery of ancient stone circles. One of the oldest is the Ring of Brodgar on Orkney, probably a creation of the culture that later built Stonehenge. Most guidebooks assert that the 21 currently standing stones (8 of them re-erected between 1906 and 1908) are the remnants of a circle of 58 or 60 stones.

The trouble is, this common assertion just isn’t true. There is no sign that there were ever more than 40 standing stones in the Ring – the latest archaeology, using a range of techniques, cannot find evidence for more than 16 sockets for stones other than those still standing. The modern mind has extrapolated from the stones that remain and calculated how many there would be if there had once been a circle of that circumference made up of stones with similar gaps between them (and ignoring the fact that the gaps vary). But that wasn’t the point for the ancient mind. Our ancestors thought differently from us, sometimes in ways that are even odder to our modern eyes: some stones weren’t ever deeply planted in the ground and so may have fallen very quickly.

The point is that the Ring of Brodgar wasn’t a thing, it was a doing: for our ancestors it was the collective action that mattered, its creation, not so much the resulting thing. Brodgar was a community event that brought people together in a shared effort. The stones aren’t matching: they come from different spots around the islands (at least 7), presumably transported by different families the miles from their best quarry, and raised as part of a communal effort. The ditch around the stones was certainly dug in small patches that were then joined together, perhaps further evidence of the bonding process of each family doing its own portion of the work before they were brought together as a unified whole – overall a work requiring an estimated 80,000 person hours.

The Ring of Brodgar, both stones and gaps between them

It’s like Peru’s ancient Nazca lines, about which modern people, flying over them in aeroplanes, puzzle as to the creation of images that can only be seen from above in this way. Most archaeologists now agree that the Nazca images were ceremonial paths, walked by people on special days or for particular reasons. They were not meant to be seen but to be experienced, perhaps to be made anew. The Nazca lines too were a doing, not a thing.

I keep coming back to these thoughts as I read a thoughtful and thought-provoking recent book, Don’t Talk About Politics. Author Sarah Stein Lubrano notes that we fail to persuade each other on politics and are wasting time and energy in talking at – and past – people with whom we disagree. Her core point is that politics is a doing, it is something that we need to participate in rather than see as separate to us, as something about which we can debate while remaining dispassionate observers: “To think effectively about politics…is not only to think about action; it is also, by necessity, to take action. Good political reasoning cannot happen simply by reading and debating.”

She goes on:

“When it comes to politics, we’ve probably placed too much societal emphasis on words and too little on action. Many people would say that democracy is about whether people can make up their own minds and then vote. But this is, in fact, a fairly passive idea of political involvement…our collective common sense of what politics is has, I’d suggest, become hollowed out. It involves too little of what truly changes people, their priorities and their actions.”

Stein Lubrano’s focus is politics, but society too is a doing, and so is the economy. We need to be active participants in both, and dangers lie where many members of a population are not. And at present, too many people do not feel like active participants in either the society or the economy.

This thought process echoed for me across a recent discussion co-hosted by my friends at the Fairness Foundation. They’ll write more fully and directly on what was a discussion under the Chatham House rule, so I will stick with my reflections. The core of the conversation centred on the issues I touched on in An Inequality in Dignity, or the Dignity Deficit; one participant talked about there being a ‘crisis of belonging’ that we all need to seek to address actively.

We discussed the way in which many people currently feel profoundly uninvolved in the economy. It isn’t just that they own little and lack a stake in the economy; more, they feel that the economy is something that occurs elsewhere in which they are not engaged. They lack both belongings and belonging. The unfairness embedded in the current economy, where so many are have-nots, is profoundly alienating and destructive of human dignity. Similarly, a dignity deficit arises because people do not feel they have a place in society, that their voices are not heard and will not be heard, that they have no agency. They withdraw into fury and anger because they feel that they no longer have a place in which they are welcomed as belonging.

This is true in the economy and in society more broadly, and the tensions and disconnects it fuels are plain to be seen. Stein Lubrano devotes a whole chapter to the psychological side of these sentiments. She refers to it as social atrophy, a sense that everyone is becoming isolated, detaching themselves from society and community. She notes the disastrous consequences that arise. As she points out, this is a much more fundamental risk than the way it is usually discussed, as an individual crisis of loneliness; it is a broader communal fracturing. “We may…distrust society more not only because it no longer provides everyone with what they need, but also because, as we become more isolated, the suspicious and paranoia-inducing structures in our brains become more and more activated,” she argues.

If we are to address the dignity deficit, the crisis of belonging, we need to involve people, we need for them to feel that society and the economy (and yes, politics too) is something in which they have a role to play, that these are not just issues that happen elsewhere between other people, but rather that they can act and be engaged. That will require more physical venues for people to meet face to face, for society physically to thrive. It will require a democratisation of finance, so that ordinary people understand that they do literally have a stake in the economy and are economic actors in their own right – an understanding that their pension savings make them part-owners of assets and of companies around the world. This needs to be understood as giving them agency, the scope to be involved and to act, not simply to be onlookers at activity involving others.

It turns out that our ancestors were right: society is a doing, it isn’t about things. We need to get out of the trap of the modern mind, that emphasises the thing rather than the doing. We need less emphasis on belongings and more on belonging.

I am happy to confirm as ever that the Sense of Fairness blog is a purely personal endeavour

Landscapes Revealed: Geophysical survey in the heart of the Neolithic Orkney World Heritage Area 2002-2011, Amanda Brend, Nick Card, Jane Downes, Mark Edmonds, James Moore, Oxbow, 2020

Building the Great Stone Circles of the North, Colin Richards (ed), Windgather, 2013

Don’t Talk About Politics: How to Change 21st Century Minds, Sarah Stein Lubrano, Bloomsbury Continuum, 2025

The media has reported that Meta (the Facebook, Instagram and WhatsApp company) has won a legal case on the use of copyrighted materials in training its AI models, that the use of copyright materials was a ‘fair use’. As often with the law, it’s a bit more complicated than that.

The case in question was Kadrey v Meta, and summary judgement was released last week (the judge, Vince Chhabria, deciding on the basis of arguments that the case did not need to go to jury trial because the plantiffs had not made a convincing case, enabling Meta to succeed in a call to dismiss it). The legal question at issue was whether the accepted abuse of copyrighted works in training AI amounts to a ‘fair use’. As well as considering fairness, the case opens a wider window on AI.

Before delving, I will note that I’ll continue to use the term AI, because it’s used in the case and the term is in general use for these emerging new technologies. But as both recent books The AI Con and AI Snake Oil (the two latest additions to my bookshelf) start off by making clear, there is no such single thing as AI. It is a catch-all term for a range of technologies – some of only very dubious effectiveness – and is really just a brand that is being deployed to raise (enormous amounts of) funding (two headlines from the Financial Times over this weekend cast light on the scale of this financing: Meta seeks $29 billion from private credit giants to fund AI data centres, and Nvidia insiders cash out $1 trillion worth of shares). The best known, and most used, of these new AI technologies are called large language models (LLMs), accurately described as stochastic parrots: models that simply put one word after another according to statistical models developed through their training.

Many legal systems favour the term fairness, and ‘fair use’ is a well-established concept in US law. The country’s Copyright Act (in 17 USC §107) clearly restricts fair use to usage “for purposes such as criticism, comment, news reporting, teaching (including multiple copies for classroom use), scholarship, or research”. It sets out four factors that should be considered in determining whether a given use is in fact fair:

1. the purpose and character of the use, including whether such use is of a commercial nature or is for non-profit educational purposes; 2. the nature of the copyrighted work; 3. the amount and substantiality of the portion used in relation to the copyrighted work as a whole; and 4. the effect of the use upon the potential market for or value of the copyrighted work.

Deciding what uses are fair is both a matter of law and of the specific facts, meaning that there are multiple cases that have considered these factors. The list of four factors is not exhaustive, but are assistants in reaching the overall conclusion. The fourth factor, whether the use risks substituting for the copyright materials in the marketplace, is generally seen to be the most important. Courts need to apply judgment and consideration is deciding on fair use; as ever, assessing fairness requires thought and judgment.

As judge Chhabria explains in his summary judgement:

“What copyright law cares about, above all else, is preserving the incentive for human beings to create artistic and scientific works. Therefore, it is generally illegal to copy protected works without permission. And the doctrine of “fair use,” which provides a defense to certain claims of copyright infringement, typically doesn’t apply to copying that will significantly diminish the ability of copyright holders to make money from their works.”

He is as rude as a judge ever gets about a fellow judge who reached a recent decision on a fair use case in relation to Anthropic, another AI firm (Order on Fair Use at 28, Bartz v Anthropic PBC, No. 24-cv-5417 (N.D. Cal. June 23, 2025), Dkt. No. 231). That judge was convinced by the argument that training AI was no different from – and had no more impact on the market for copyright products – than training schoolchildren to write. Chhabria says: “when it comes to market effects, using books to teach children to write is not remotely like using books to create a product that a single individual could employ to generate countless competing works with a miniscule fraction of the time and creativity it would otherwise take. This inapt analogy is not a basis for blowing off the most important factor in the fair use analysis.”

And surprisingly given his overall ruling, Chhabria is very clear that AI companies are breaching copyright law and are damaging the commercial market for copyrighted works. He seems very sure that AI companies fail at the fourth factor in assessing fair use: “by training generative AI models with copyrighted works, companies are creating something that often will dramatically undermine the market for those works, and thus dramatically undermine the incentive for human beings to create things the old-fashioned way”.

Chhabria also notes a simple flaw in one of the AI companies’ arguments: that applying copyright law will stifle the development of this technology. He notes that any finding that this use of copyrighted materials isn’t fair use does not bar that use, it just requires that AI companies need to reach a commercial agreement with copyright holders to compensate them for the – unfair – use of their materials. As he points out, these businesses project that they will make billions, indeed trillions, of dollars from AI services, so should be able readily to afford such licensing. Indeed, the court saw evidence that Meta initially sought to licence book materials for training purposes, and considered spending up to $100 million on doing so. This never happened because book publishers do not hold rights to this use of book materials – like other novel uses, the rights rest with the authors – so there is no central point or points for such a negotiation. The fact that AI companies are seeking direct commercial benefit from their use of copyright materials makes their burden in demonstrating fair use much harder.

Despite Chhabria’s conclusions that seem to strongly favour the copyright-holders who brought the case, he nonetheless found against them. The copyright holders are 13 authors who argued that their works had been used in training Facebook’s Llama LLM models. In essence they failed in their claim because their lawyers focused their efforts and arguments in the wrong place. They made their arguments predominantly under the first three of the four factors in §107 of the Copyright Act, and failed in those. While the fourth factor – the effect of the use on the potential market for the copyrighted work – is generally seen as the most important, that is not an argument they made strongly. They simply did not argue (or were at best “half-hearted” in those arguments) that their works had been used as the basis for a tool which might flood the market with similar works, undermining the value of their copyright, nor did they provide evidence to support such an argument. This was “the potentially winning argument” according to Chhabria; the (weaker) points actually deployed in argument before the court did not succeed.

Chhabria was clear:

“this ruling does not stand for the proposition that Meta’s use of copyrighted materials to train its language models is lawful. It stands only for the proposition that these plaintiffs made the wrong arguments and failed to develop a record in support of the right one.”

It does seem ludicrous that the most valuable companies in the world should argue that it is fair for them to take stolen copies of books subject to copyright protection (the training materials were taken from so-called ‘shadow libraries’, of illegally scanned books) and make what they predict will be huge commercial profits as a direct result, while providing the copyright holders with no compensation. The fact that Meta explored licensing but found it too difficult and delaying helps support the case that this would be the right thing to do.

The Kadrey case reports one other specific element of the training of Llama models – that they are taught not to produce more than 50 words together that are repeated from any one source (even if provided with highly directive prompts to do so). The fact that this is a deliberate part of the training shows just how prone these technologies are just to leaning on what they have read. In a recent Financial Times interview, Professor Emily Bender, coiner of the term stochastic parrots and co-author of both the academic article that brought the term to prominence and of The AI Con, is quoted as calling LLMs “plagiarism machines”.

I have to admit that, as may be apparent from my recent reading habits, that I am an AI sceptic. I suspect that we will look back on this period with puzzlement, and wonder why we threw colossal amounts of computing power – and colossal levels of energy in our carbon-constrained world – at jobs that human brains are better at. AI is neither artificial nor intelligent: it isn’t artificial because it depends on human creativity in the training, and it also depends on significant, horrible, labour (typically cheap precarious labour in emerging economies) in cleansing the models of the filth that it produces because it has been trained on, among other things, the global sewer that is the Internet. It isn’t intelligent, it’s just reproducing others’ language patterns based on statistics, “haphazardly stitching together sequences of linguistic forms it has observed in its vast training data…without any reference to meaning” as the stochastic parrots paper put it. As Bender told the FT, we are “imagining a mind behind the text…the understanding is all on our end”. There will no doubt be jobs that AI technologies are useful for, but like any human tool it is tailored to its task, and not a general purpose vehicle for all activity. Currently we have a hammer and are making the mistake of seeing everything as a nail.

As a result, I suspect that much of the billions being deployed in AI currently will turn out to have been wasted. I should admit also that my view may be coloured by the fact that I entered the investment world exactly at the time of the dotcom bubble. While I avoided losing money in the dotcom bust, I also missed out on investment gains as that bubble inflated.

But this is a blog on fairness, not AI cynicism. The Kadrey decision did not conclude that Meta’s actions were fair, only that the copyright-holders had failed to deploy the arguments that might have shown how unfair the use of their materials was. This will clearly not be the last such case, and while the AI businesses will continue to deploy some of their investors’ millions into their defence, judge Chhabria’s legal conclusions suggest they will have a challenging time winning cases argued on the right basis.

Rather than finding that Meta’s use was fair, the Kadrey decision is highly suggestive that AI is not fair in its use and abuse of copyright materials. That feels right: fairness should always tend to rebalance power away from those with billions towards those of whom they take uncompensated advantage.

I am happy to confirm as ever that the Sense of Fairness blog is a purely personal endeavour

Kadrey v Meta, Case No. 23-cv-03417-VC, Summary Judgement 25 June 2025 (Docket Nos 482, 501)

The AI Con: How to Fight Big Tech’s Hype and Create the Future We Want, Emily Bender, Alex Hanna, Bodley Head, 2025

AI Snake Oil: What Artificial Intelligence Can Do, What it Can’t, and How to Tell the Difference, Arvind Narayanan, Sayash Kapoor, Princeton University Press, 2024

Reading an old book can sometimes feel like an archaeological dig – you find fragmented artefacts of how people used to think and have to try to piece together an understanding of their world, and their world view. Very often it serves to illuminate our own.

That’s definitely my sense while reading a book called Equality by an old socialist and economic historian, RH (Richard Henry) Tawney. My edition dates from 1964 but the original book was published in 1931, based on lectures given in 1929. This version enjoys a 1964 introduction by founding father of social policy Richard Titmuss, and no fewer than two prefaces by Tawney himself, one from the 1951 revised edition and one from the ‘substantially revised’ 1938 edition. Reading through these in this order is like uncovering historic layers of English inequality, and repeated aspirations for greater equality. What’s more, the first chapter of the book, The Religion of Inequality, starts by referring to a lecture by Matthew Arnold from I think 1878, to which it attributes the coining of that phrase.

I find it impossible to read these archaeological artefacts and not reflect on our own age. This blogpost aims simply to capture a few sentiments from each of these layers of history. Readers will no doubt be conscious of the great ruptures and attempts towards greater equality that provided the context for the writing of each of these layers of commentary, from the heights of the Cold War, the challenges of the Second World War and the creation of the welfare state that followed it, the Great Depression and the rise of fascism – and even, back around the 1870s, the first steps to broad enfranchisement (and while the right to vote did not then extend to women, that decade did see them permitted for the first time to retain their own property rather than simply surrender it on marriage).

Titmuss in his 1964 introduction:

“We…delude ourselves if we think we can equalize the social distribution of life chances by expanding educational opportunities while millions of children live in slums without baths, decent lavatories, leisure facilities, room to explore and the space to dream. Nor do we achieve with any permanency a fairer distribution of rewards and a society less sharply divided by class and status by simply narrowing the differences in cash earnings among men during certain limited periods of their lives.”

“Long years of economic depression, a civilians’ war, rationing and ‘fair shares for all’, so-called ‘penal rates’ of taxation and estate duty, and ‘The Welfare State’ have made little impression on the holdings of great fortunes…Wealth still bestows power, more power than income, though it is probably exercised differently and with more respect for public opinion than in the nineteenth century.”

“These consequences of technology in an age of abundance are more likely to increase than to decrease differentials in income and wealth if no major corrective policies are set to work…Without a major shift in values, an impoverishment in social living for some groups can only result from this new wave of industrialism.”

Tawney in his 1951 preface:

“Like earlier wars of religion, the credal conflicts of our day will find varying issues in different regions; but, if Europe survives, societies convinced that liberty and justice are equally indispensable to civilization will survive as part of her. The experience of a people which regards these great abstractions, not as antagonists, but as allies, and which has endeavoured, during six not too easy years, to serve the cause of both, is not barren of lessons which may profitably be pondered.”

And he quotes The Times from 1 July 1940:

“If we speak of democracy, we do not mean the democracy which maintains the right to vote, but forgets the right to live and work. If we speak of freedom, we do not mean a rugged individualism which excludes social organization and economic planning. If we speak of equality, we do not mean a political equality nullified by social and economic privilege. If we speak of economic reconstruction, we think less of maximum production…than of equitable distribution.”

Tawney in his 1938 preface:

“It is still sometimes suggested that what Professor Pigou, in his latest work, calls ‘the glaring inequalities of fortune and opportunity which deface our present civilization’ are beneficial, irremediable, or both together. Innocent laymen are disposed to believe that these monstrosities, though morally repulsive, are economically advantageous, and that, even were they not, the practical difficulties of abolishing them are too great to be overcome. Both opinions, it may be said with some confidence, are mere superstitions.”

“Institutions which enable a tiny class, amounting to less than two per cent of the population of Great Britain, to take year by year nearly one quarter of the nation’s annual output of wealth…are an economic liability of alarming dimensions. They involve…a perpetual misdirection of limited resources to the production or upkeep of costly futilities, when what the nation requires for its welfare is more and better food, more and better houses, more and better schools.”

“Today, when three-quarters or more of the nation leave less than £100 at death, and nearly two-thirds of the aggregate wealth is owned by about one per cent of it, inheritance is on the way to become little more than a device by which a small minority of rich men bequeath to their heirs a right to free quarters at the expense of their fellow-countrymen. The limitations imposed on that right during the past half-century were greeted, when first introduced, with the usual cries of alarm; and the alarm, as is not less usual, has been proved by experience to be mere hysteria. It is perfectly practicable, by extending those limitations and accelerating their application, to reduce the influence of inheritance – at present a strong poison – to negligible dimensions.”

“To make [democracy] a type of society requires an advance along two lines. It involves, in the first place, the resolute elimination of all forms of special privilege, which favour some groups and depress others, whether their source be differences of environment, of education, or of pecuniary income. It involves, in the second place, the conversion of economic power, now often an irresponsible tyrant, into the servant of society, working within clearly defined limits, and accountable for its action to a public authority.”

Tawney reports that Matthew Arnold said, in c1878:

“Arnold observed that in England inequality is almost a religion. He remarked on the incompatibility of that attitude with the spirit of humanity, and sense of the dignity of man as man, which are the marks of a truly civilized society. ‘On the one side, in fact, inequality harms by pampering; on the other by vulgarizing and depressing. A system founded on it is against nature, and, in the long run, breaks down.’”

As LP Hartley says in another old book, one that deliberately plays with memory and history, “The past is a foreign country; they do things differently there.” But often ‘they’ worried about the same challenges we do, and sought similar solutions.

I am happy to confirm as ever that the Sense of Fairness blog is a purely personal endeavour.

It’s no criticism of the other presenters at a recent seminar on political populism hosted by King’s College London’s Policy Institute and the Fairness Foundation – it was a consistently energising discussion – that (for me at least) the most striking comment was this from Liam Byrne MP:

“There’s a real inequality of dignity [in the UK] today. People who were prepared to fight for the dignity of working people would go a long way [politically].”

Byrne chairs the House of Commons Business & Trade Select Committee and went on to describe the committee’s recent work. In particular, he has been struck by the strong public reaction to the Committee challenging companies that are seen to have been acting unfairly. He sees this as evidence of a real thirst for a body that seeks to inject more fairness into the relationship of business with society.

This blog is of course all for such an injection of fairness, but this post in particular is about the question Byrne raises about the inequality in dignity. What might we mean by the term, and how might we address that particular area of inequality, of unfairness?

Fortunately, there’s an academic who has dedicated her career to considering dignity, who is permitted to benefit from it, and how it can be reinforced. She is Michèle Lamont, Professor of Sociology and of African and African American Studies and the Robert I Goldman Professor of European Studies at Harvard University. A proud French Canadian, she feels a profound affinity with those at the periphery of societies. Her work largely focuses on the US, but she collaborates internationally and the lessons to be learned are global.

Lamont says at one point in her latest book, Seeing Others, that it is an “exploration of how we decide who matters”; that description really applies to most of her work. The phrase for me is both encouraging and profoundly unsettling at the same time. If we are to deliver the equality of dignity that Byrne is in effect seeking then we need all people to matter, not just those we decide are worthy of dignity. That is Lamont’s aspiration too, but she recognises the reality that we are far away from that point currently: it’s not by chance that the subtitle of Seeing Others is How to Redefine Worth in a Divided World.

Seeing Others is mostly focused on further-educated members of Gen Z and their efforts to recognise the worth of others. Byrne discusses their deliberately inclusive disclosure of pronouns, which has become such a target for some – opponents of the approach ironically seeing it as exclusionary, in contrast to its inclusive intentions. But earlier work was more directly concerned with the perspectives of the working class – in particular The Dignity of Working Men.

Lamont’s core finding in that book is that people create their own framework of dignity for their lives, and the camaraderie of working life together reinforces it. Morality lies at the heart of this sense of self, in the form of straight-talking honesty and a strong self-discipline – importantly, these are characteristics that they believe are lacking in many of their bosses and those of higher social status (they are only partly believers in American meritocracy). Lamont finds that “morality plays an extremely prominent role in workers’ descriptions of who they are and, more important, who they are not. It helps workers to maintain a sense of self-worth, to affirm their dignity independently of their relatively low social status, and to locate themselves above others.” Providing for and protecting their family lies at the core of this moral life, not least because it is “a realm of life that gives them intrinsic satisfaction and validation – which is crucial when work is not rewarding and offers limited opportunities”.

Byrne himself in his excellent recent book The Inequality of Wealth doesn’t much deal with these issues of dignity. Subtitled Why it matters and how to fix it, the book is much more trying to develop a prescription for addressing broader unfairness in our society. But there is one discussion that is very relevant. Tellingly in a chapter called The Cost of Affluence, Byrne discusses the work of psychologist Dacher Keltner, whose experiments explore the sense of fellow feeling and the willingness of strangers to support one another. He quotes Keltner as saying: “we’ve done several studies that look at how your wealth, education and prestige of your career or family predict generosity. And the results are consistent: poorer people assist other people more than wealthy people.” Here too is a source of dignity – and also an indication that working people are right to be cynical about the morality of those better off than themselves.

The Dignity of Working Men was published in 2000, but its interviews date back to 1992 and 1993. And some of the comments feel all of their 30-plus years of age. In particular, this comment from postal worker Steve Dupont, who argues with his immediate boss on a regular basis, feels like it comes from a very distant time: “This has gotten me in trouble but as I always say to [my foreman], ‘I can always find another job, I can’t always recoup my pride and my own dignity.’” There may have been an element of bravado then, but now not even the most bragging of working men would feel able to assert their ability always to find another job.

And that seems to be the core of the dignity deficit: when the ability to stand up for what is right, when self-discipline isn’t enough to avoid being restructured out of employment, then there is little basis for this traditional source of dignity and pride. Where it is no longer possible, even with hard work and discipline, to protect and provide for one’s family, dignity becomes less possible too.

One consequence of this dignity deficit is a nationalistic fervour. In The Dignity of Working Men, Lamont finds that “Being an American is one of the high-status signals that workers have access to”. She amplifies this finding in Seeing Others: populist political messages “extend to downwardly mobile people one of the few high-status identities available to them: their “winning” status as Americans”.

There’s a danger if this loss of dignity goes too far. A sense of humiliation is probably the opposite of the sense of dignity. And humiliation is a dangerous feeling. A recent excellent paper published by the wonderful people at Psyche discusses the impacts of humiliation at a national level – or at least the impacts of narratives of national humiliation. These are the fuel for conflict, finds author Raamy Majeed (a lecturer in philosophy at the University of Manchester). His title, Does national humiliation explain why wars break out?, expresses where the loss of dignity may end. “When citizens of a nation feel humiliated, they become more likely to support aggressive foreign policy initiatives.” Fairness (naturally!) can lean against this sense; Majeed reports on the work of philosopher Avishai Margalit, especially in The Decent Society, which “argues that a just society does not necessarily prevent its citizens from feeling humiliated but instead avoids creating humiliating conditions”.

Even short of conflict, there are direct physical consequences of the inequality in dignity. In Seeing Others, Lamont makes a clear link to the work of Anne Case and Angus Deaton on deaths of despair: “dignity affects quality of life just as much as material resources do”.

So we need to address the dignity deficit. A just society will help limit humiliation, but are there other prescriptions from Lamont’s work? She attempts exactly that in her conclusion to Seeing Others, a chapter entitled Strengthening our Capacity to Live Better Together, and she is exploring it in her current work, which she calls a study of the three Manchesters (Oldham, near Manchester in the UK; Greater Manchester, New Hampshire; and Tampere in Finland, nicknamed the Manchester of the North; all former centres of industry). At a talk this month at the London School of Economics, Lamont discussed both Seeing Others and this three Manchesters work, which is considering how working class 18-30 year olds seek and gain recognition – another term for dignity perhaps – and the role of place, history, politics, exclusion and inclusion in that.

It’s too early to have conclusions from the Manchesters work, but the conclusion to Seeing Others does provide some insight. Much of this is relatively vague, emphasising the need for shared visions, hopes and narratives – and at its most simple, shared existences, rather than living very segregated lives. There is a hint at emphasising the proud inclusivism in national stories, rather than the exclusive aspects of them. Lamont also calls for the middle-classes not to ‘opportunity hoard’ as much as they (I should say we) do. She gets more specific when she says (without acknowledging the element of division she is encouraging):

“The Democratic Party could make significant gains by regaining working-class voters with not only redistributive policies, but also with messages of solidarity and dignity, as an alternative to the Republican Party’s populist messages of division and blame. Redirecting working-class anger toward the one percent is more likely to sustain fruitful alliances than driving wedges between diverse categories of workers who have so much in common.”

In the absence of such efforts, and the absence of efforts to build a shared sense of community, it may be no surprise that a lack of fairness in dignity, echoing wider unfairness in society, is fuelling political and social tensions. Many people have the sense that the status status quo isn’t working for them, and are willing to see dramatic change as a result. Byrne is right, we need to be working to close the dignity deficit, to instil a greater fairness, an equality, in dignity.

I am happy to confirm as ever that the Sense of Fairness blog is a purely personal endeavour

AO Smith, a 150-year old family-dominated US company that manufactures water heaters and boilers, held its Annual General Meeting (AGM) last week. The Milwaukee-based company chose to hold the meeting at the National Association of Manufacturers in Washington DC.

One issue that faced the shareholders for consideration at the meeting was a resolution proposed by a fellow investor, NorthStar Asset Management. Headlined Eliminating Discrimination through Inclusive Hiring, the resolution was actually much more precisely focused than this slightly generic title indicates. The resolution called on AO Smith to consider afresh its hiring policies and practices to ensure that they appropriately consider people with records of having been arrested or imprisoned (technically, to meet the strictures of US regulation, the resolution is framed as seeking a report on these matters, but the intent is clear).

Such recruitments are known in the US, wonderfully, as ‘fair chance hires’.

One reason they are called fair chance hires is because of the racial discrepancies in imprisonment in the US. Blacks are around 14% of the US population but are 39% of its prison population (it isn’t clear how Hispanics are treated in the prison population data, but even if they were to be included in that ‘Black’ percentage, the over-representation is still 39% against around 30%). Similarly, Native Americans are around 1.5% of the overall population but 3% of those in prison. As NorthStar’s statement regarding its shareholder proposal states: “As people of color are disproportionately incarcerated, pursuing fair chance employment can also advance company diversity goals.”

The fund manager quotes AO Smith’s ambitions around diversity, as stated in previous annual reporting, and contrasts this with an apparent lack of progress on gender diversity as well as racial/ethnic diversity. It goes on to argue: “Shareholders believe that company value would be well-served by examining whether revisions to company practices related to recruiting formerly incarcerated individuals could decrease future risks related to discriminatory hiring.”

It’s the second year in a row that NorthStar has proposed such a resolution. According to its own website, in 2024 the proposal garnered 6.6% support. At a headline level, the voting results released this week seem to suggest that this year the asset manager was less successful, with around 5.5% of shareholders declining to back the company on the issue (this number aggregates those abstaining with those who supported the resolution outright). But because there are two classes of shares, and the Class A shares with 10 times the voting rights are almost entirely in the hands of the founding Smith family, the actual voting among shareholders other than the Smiths was more favourable: around 19.3% of the broader shareholder base appears to have backed the resolution (or at least to have not opposed the resolution). This is a notably high result given that many larger mainstream fund managers have reduced their support for shareholder resolutions in recent years. NorthStar proposed similar resolutions at three other companies last year, including Adobe; whether any others beyond the one at AO Smith make it to the ballot in 2025 remains to be seen.

The concept of ‘fair chance hires’ isn’t an international one. But there is a UK company with a proud record of hiring ex-offenders: another long-standing (160 years in its case) and eponymous family firm, Timpson. The retailer, famous for key-cutting and shoe repairs, proudly reports that 12% of its 4500 staff have a past criminal conviction. It provides training in prison, and has colleagues who are on Release on Temporary Licence (often referred to as day release), seeking to make the return to life outside prison more smooth. “We strongly believe in giving people a second chance in life,” Timpson asserts. This appears to work for the business: it reports that 75% of ex-offenders stay long-term with the business.

While the company has celebrated its sesquicentenary, the approach to recruiting offenders is much younger. It dates to 2002 and a visit to prison by CEO John Timpson. Timpson built a rapport with a guy called Matt, and hired him when Matt was released. But it’s now a significant part of the business: the corporate foundation spends over £1 million a year to support the employment of ex-offenders, and ‘Inclusion’ is one of five principles on which the business culture is built (the others are also wonderful words: Trust, Kindness, Loyalty, Generosity). The full principle reads: “We’re proud to employ people who find job hunting really tough, and 12% of our new recruits actually come from prison.”

There are huge positive externalities from this sort of activity: the value to the business of these loyal staff members is nothing to the value to society of successfully reintegrating those released from prison. The government’s own estimates put the cost of reoffending at over £18 billion, and the UK – like the US – has a poor record of supporting prisoners to train or to find any alternative way of making a living beyond crime.

Prison is only temporary for all but the worst offenders. We need to be better at rehabilitation, and we need to do more to reduce recidivism. We need more second chances, and more fair chance employers.

I am happy to confirm as ever that the Sense of Fairness blog is a purely personal endeavour

‘Beyond the regulatory boundary, “fairness” can be seen as an opportunity to generate value to both the enterprise and its wider community. Fairness frameworks can be aligned with corporate and brand values as part of the broader enterprise strategic and risk management framework.’

While the starting point for a recent report on fairness in health insurance is the regulatory consumer duty recently put in place by the UK’s Financial Conduct Authority (FCA), it’s clear that the paper is more interested in business risk and opportunity than in mere regulation. As this blog has long found, there are remarkable numbers among the challenges that modern business faces that can best be viewed through the lens of fairness – and many opportunities that can be uncovered by deploying that lens.

From those smart people at Milliman, the report, Fairness in UK health insurance: Developing a framework and best practices in health insurance, covers the full range of relevant issues. These include: fairness in the delivery of consumer relations, especially the treatment of vulnerable customers; fairness in the application of new technologies, including AI and algorithms; and considerations of structural biases in healthcare.

While the report is narrowly focused on health insurance, it naturally considers many of the wider fairness issues that apply in the field of health. Foremost amongst this is the sterling work of the wonderful Sir Michael Marmot (perhaps most accessibly in The Health Gap). Marmot’s consideration of the social determinants of health is reflected in this brief segment of the report:

‘With greater focus on protected characteristics, there has been a move to greater use of “lifestyle” factors as personal “choices.” ‘Certainly, smoking is widely accepted as a choice. Possibly exercise; but are postcode, income, occupation, education, children? Whilst at some point they may have been “choices”, at later points in life they may be fixed rather than changeable (or controllable).’

Marmot shows that many of these issues are not choices at all, but are the outcomes of inequalities in wider society. In brief, poor housing, work, education, income, are all among the clearest determinants of poor future health outcomes. Few of these are chosen, particularly in economies where meritocracy is failing. While people in poverty are unlikely to be accessing health insurance, Marmot’s analysis raises questions about how fair it might be to consider some of these lifestyle issues in the pricing of such insurance.

The use of technology in relation to healthcare is also a significant feature of the Milliman work. In particular, the paper argues that: “Greater personalised medicine and healthcare are likely to mean that trust, privacy and fairness are increasingly necessary parts of ensuring good customer outcomes.” Further, it is not enough that fairness be done, it must be demonstrable that it has been delivered in practice: “Risk-based pricing and underwriting approaches should be auditable with clear accountability and robust governance of decision-making processes.” It is certainly not enough to assume that AI or algorithms will generate fairness – as this blog has found previously, these technologies can encode and replicate pre-existing unfairnesses.

But it is in dealing with the FCA’s consumer duty requirements that the paper breaks most fresh ground. Given that these requirements are still new, we have not yet seen best practices developed. The paper is therefore one of the earliest detailed expositions that I have seen of how it might bite in practice, and what it may require of business. The Milliman summary of the application of the duty to health insurance seems clear and wholly appropriate to me:

“For UK health insurers this combines providing fair customer treatment and clear information with products that genuinely meet their needs. Particular attention is required to product design and suitability, customer communication, customer support and providing “fair value” as well as systems to track performance and make adjustments. There is also a need to give special attention to vulnerable customers.”

The paper later considers some of the detailed best practices that seem likely to be required under the duty, including “Being transparent with customers, in particular with terms and conditions around the inclusion or exclusion of pre-existing medical conditions, any moratorium and exclusion of any specific types of treatments (often highly complex, severe conditions)” and “Being clear and signposting these policies using laymen terms in the policy documentation so there is no ambiguity.”

And there is a particular need for fairness in the area of health insurance, a particular need for care regarding consumer duty. As the paper point out: “Almost all customers making health claims are vulnerable to some extent, with particular efforts required to meet the needs of the most vulnerable.”

Reinsurance firm Pacific Life Re was also recently inspired by the advent of the FCA consumer duty regime to consider the uneven distribution of insurance products across different communities. But its response is a rather more bluntly commercial one: “Understanding where communities are underserved, both within your own business, and that of the industry, offers an opportunity.” This has echoes of the fortune at the bottom of the pyramid thinking that seems slightly to have slipped from much business thought. But as the work of Citizens Advice continues to show, accessibility and pricing of various insurance products are not evenly distributed across consumer groups.

The Milliman paper also draws a fascinating analogy to the independent governance committees that are in place in the pensions provided by insurance companies. These IGCs have responsibility for overseeing the customer experience and defending consumer interests, with particular attention to value for money. The paper suggests that there is something in this model that would be worthwhile perhaps extending to health insurance: “We consider that these efforts can be a best practice governance framework for the health insurance sector and help tap into consumer groups’ understanding of “fairness” and how their expectations evolve over time.” IGCs are consumer champions in pensions – do we need something similar for other products?

For some, the very availability of commercial health insurance in the UK is itself a symbol of unfairness. Where there is (at least in theory) universal provision through our National Health Service, health insurance can often be seen as jumping the queues which seem the main form of rationing of that provision (and which can make its universality seem theoretical). But we have to recognise the reality of the use of health insurance – not least as a standard employee benefit from companies keen that their staff stay healthy. It is certainly better that it is deployed fairly than not. The Milliman paper provides a pathfinder for that, as well as useful insights into the consumer duty more broadly.

Readers (at least those that read the small print at the foot of every blogpost) will know that the Sense of Fairness blog is a purely personal endeavour. But naturally I am sometimes inspired to write things by events in my working life.

So it is this week, following a gathering on Tuesday hosted by fund manager Impax on the role of corporate culture in business performance. Naturally, the firm has a product to sell and wants to demonstrate its prowess in identifying share price performance drivers in what is still a surprisingly under-researched area.

Impax showed us striking charts showing stronger performance by companies with better culture, on the metrics that they have been able to garner from company reporting and more independent sources on employee satisfaction such as Glassdoor. Note that of course I am not making any investment recommendation.

Perhaps more striking than the performance statistics were the anecdotes from active fund manager Charles French, who relayed stories from the front line of asking CEOs about culture. As I too used to find when I asked my favourite “How are your people?” question, the range of responses to questions about culture tells you a great deal about the attitude and mindset of bosses. Some literally have nothing to say and do not know how to begin an answer; others become energised and demonstrate very clearly how much of a focus for them is inspiring their staff. You are left in no doubt which bosses – and so businesses – you would prefer to work for.

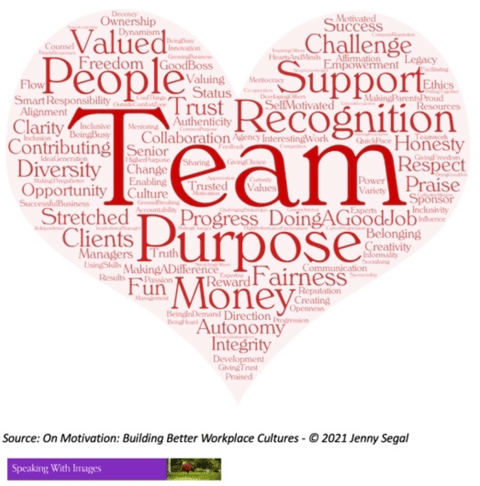

The event also featured a presentation and panel discussion on corporate culture. The panel featured a couple of my favourite people who have done great work on corporate culture, Tina Mavraki and Annabel Gillard. Most striking for this blog were a pair of word clouds within the initial, energising presentation from Jenny Segal, whose headline offer is ‘Building better workplace cultures through creativity and understanding motivation’.

She had asked a representative group of people what motivated them at work. Fairness appears with reasonable prominence, as do a series of other words that have concepts of fairness attaching to them:

As noted in a previous post, there are very different motivations for workers at companies which have a clear purpose and seek to inspire their staff. It’s unsurprising that unfairness at work is demotivating.

Jenny also asked people what makes a good boss. Again, fairness clearly matters:

Another striking comment from the panel came from Christine Cappabianca, one of Impax’s quant team, who leads their work uncovering data on culture. Clearly the reporting dynamic around diversity, equity and inclusion factors – one of the areas she has been mining for insight – varies around the world and is shifting notably at the moment. One of the shifts that she expects to happen as diversity is downplayed is that the language of fairness will see more use, as it’s a much less divisive way of capturing the intent of these programmes. That fits with the the most forward-thinking research in this space.

Fairness matters, viscerally, to people. It’s not surprising that its presence fires us up at work and that its absence demotivates. The best managers know this viscerally too.

For subscribers to the Financial Times, there’s a great little piece (dated yesterday online so I assume in today’s print edition) on the consumer experience of algorithmic fairness and unfairness by the ever-thoughtful and thought-provoking Sarah O’Connor.

O’Connor discusses the black box experience of technology decision-making for customers – particularly in terms of being barred from access to their own accounts – which isn’t improved, or at least isn’t made any less opaque, by the application of the required human overlay if the consumer complains.

As she indicates, it’s rarely clear how fairness fits into this process.

Even given my cynicism regarding the current hype about artificial intelligence (AI)*, I have to admit that it’s very clear this new technology will transform the world of work. The societal excitement about Chat GPT and other large language models (LLMs) has been matched by corporate excitement. Companies across the world are experimenting broadly, many of them keen to deploy this as a cost-saving tool.

Of course, as with every technology shift, cost-saving comes in the form of replacing people with machinery. Efficiency means being able to do things more quickly with less human intervention. If the current experiments with AI deliver, perhaps companies will redeploy those humans to other work. More likely they will remove those people, and their costs, from their business.

That’s how business, and economies as a whole, operate: moving to more efficient ways of delivering what customers and society want, to enable higher profits or simply to enable companies to compete with rivals which are also trying to reduce their costs. On the whole, this is good for economies too as more efficiency allows national resources to the deployed to where they deliver most value.

But that redeployment takes time, and technology transitions are painful processes, for individuals and for society. Discussions of efficiency, cost savings or redeploying resources divorce us from the very real human and emotional impacts of these changes, which are of individuals losing their jobs and livelihoods, and subsequently struggling for money and self-esteem. Even where a technological shift does create new opportunities (which has been the case with every such transition previously and so seems likely once again), that takes time – time in which individuals feel unanchored, unvalued, and perhaps reach an age where further employment is unavailable to them. That can serve to destabilise society further. We shouldn’t let the economics blind us to the personal and emotional.

There is much talk in sustainable investment circles of the need for a just transition (sometimes a fair and just transition) to a decarbonised world, ensuring that care is taken to protect and support those individuals whose jobs are impacted by the dramatic shift to economic activity that must come as the world finally faces up to the realities of climate change. There is also likely to need to be a fair and just transition to an AI-enabled world.

Recent work from the International Monetary Fund (IMF) begins to open a window on this challenge, building on the sentiment of managing director Kristalina Georgieva in a blog from a year ago called AI Will Transform the Global Economy. Let’s Make Sure It Benefits Humanity. The organisation is developing approaches to consider which jobs – and which economies overall – will be impacted by the advent of AI.

Most recently, IMF staff considered impacts in Asia. A blog this month, How Artificial Intelligence Will Affect Asia’s Economies, tries to map this out in more detail, based on analysis of the breakdown of jobs in each economy. The blog reflects a deeper discussion within the analytical note attached to the Fund’s most recent Asia and Pacific Regional Economic Outlook. This analysis suggests a greater exposure to AI impacts in the region in what IMF jargon terms advanced economies, while emerging economies are likely to face lower impacts. However, they also seek to assess whether those impacts will be positive or negative for jobs: around half the impacts in advanced economies are where AI is complementary to the job, potentially driving economic benefits; meanwhile in emerging economies the majority of impacts are where there is much more likelihood of workers finding their jobs replaced. The economists hedge this analysis with language such as ‘low complementarity’ and ‘displacement’ of work, but the thinking is clear.

The language was more blunt in some earlier less detailed work, suggesting AI “could endanger 33 percent of jobs in advanced economies, 24 percent in emerging economies, and 18 percent in low-income countries”. Those conclusions look more worrying than the most recent analysis, but even the lower levels of estimated disruption are very significant.

According to the most recent analysis, there is also a gendered split in the potential impacts, again potentially exacerbating existing inequalities:

The blog reads:

“The concentration of such [complementary] jobs in Asia’s advanced economies could worsen inequality between countries over time. While about 40 percent of jobs in Singapore are rated as highly complementary to AI, the share is just 3 percent in Laos. “AI could also increase inequality within countries. Most workers at risk of displacement in the Asia-Pacific region work in service, sales, and clerical support roles. Meanwhile, workers who are more likely to benefit from AI typically work in managerial, professional, and technician roles that already tend to be among the better paid professions.”

Georgieva was clear about the risks: “In most scenarios, AI will likely worsen overall inequality, a troubling trend that policymakers must proactively address to prevent the technology from further stoking social tensions.”

The IMF economists are increasingly clear about what needs to be done about these inequality risks. According to them, a just transition will require:

Effective social security nets

Reskilling programmes for affected workers

Education and training to enable effective application of the AI opportunity, particularly for those economies where AI is currently seen to have low impacts – so that the positive benefits can be enjoyed

Regulation to promote ethical AI use and data protection

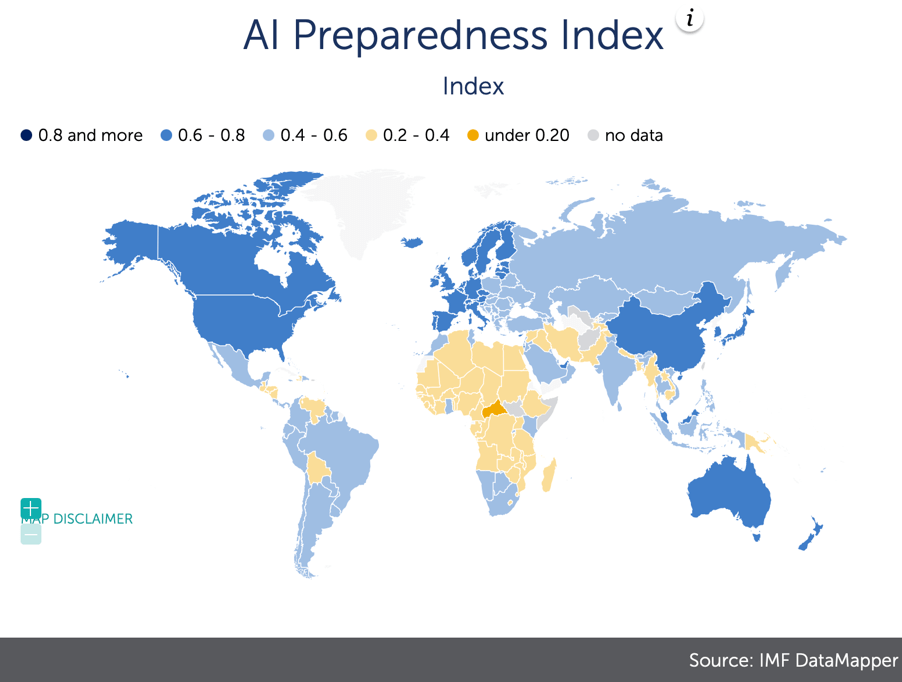

The IMF, in its AI Preparedness Index, suggests that there is a broad spread in the readiness of global economies for this coming wave of technological disruption:

Again, as things stand it seems that the greatest likelihood is for AI to exacerbate existing inequalities. Preparing for this major economic shift will demand fresh policies and investment. These are significant challenges for world economies, for companies as they embed AI into their workflows, and for global investors, to rise to.

*I have my doubts about each of the A and the I in artificial intelligence: calling an activity ‘artificial’ when it depends on the horrific grinding work of many people to scrub its results seems inaccurate; and calling it ‘intelligent’ when it is simply a logic puzzle about the likelihood of putting one word after another – the stochastic parrots as described in that prescient article (I particularly like the analogy of Emily Bender, one of the authors of that article and a professor at the University of Washington, that AI is reproducing text in the way people might if they had unrestricted access to the National Library of Thailand but without pictures or dictionaries to enable them actually to understand or translate the language). A more recent article touching on these matters is the excellent Ask me Anything! How ChatGPT got Hyped into Being, which among other things states this fundamental truth: “LLMs are not designed to represent the world. There is no understanding by the artificial agent (chatbot) of the meaning of the output it creates. It is us humans who create that meaning.” More directly, the word soups that I have been presented with by colleagues show very clearly the limits of the technology in doing anything without clear instruction and precise pre-existing materials to work with.