It is Twelfth Night, the last of the Christmas festivities and by tradition when the decorations should be taken down. But Britain’s CEOs may be tempted to leave their decorations in place and risk the threat of the goblins that apparently invites, because today is also the day when top executive pay exceeds that of the average worker — named High Pay Day by my thoughtful friends at the High Pay Centre as a way of drawing attention to these differentials in pay between CEOs and the average full-time employee.

The bad news for FTSE 100 CEOs is that High Pay moment is a full hour later than last year as it now takes a CEO 34 hours of work to surpass average annual pay rather than the 33 hours it took last year. It is not that CEO pay has reduced; it has stayed relatively unchanged. Rather, average worker pay (perhaps counter-intuitively in these times of furloughing and Covid-driven unemployment) has risen a little. This pay ratio is around 120:1. High Pay moment this year is at around 5.30, about the time this blog is being posted.

Companies are now required to disclose their own internal pay ratios, that of CEO to the company’s average-paid worker in the UK (note ‘average-paid worker’, not ‘average worker’; no worker is average), and also a comparison of CEO pay to the lower and upper quartile worker in terms of pay. These ratios were analysed in another recent publication by the High Pay Centre, at whose launch late last month I had the privilege of being invited to speak.

The results are striking, though the headline averages are lower than the 120:1 marked today:

For the FTSE 100, the median CEO/median ratio is 73:1,

and the median CEO/lower quartile ratio is 109:1

For the FTSE 350 as a whole, the median CEO/median employee pay ratio is 53:1,

and the median CEO/lower quartile employee ratio is 71:1

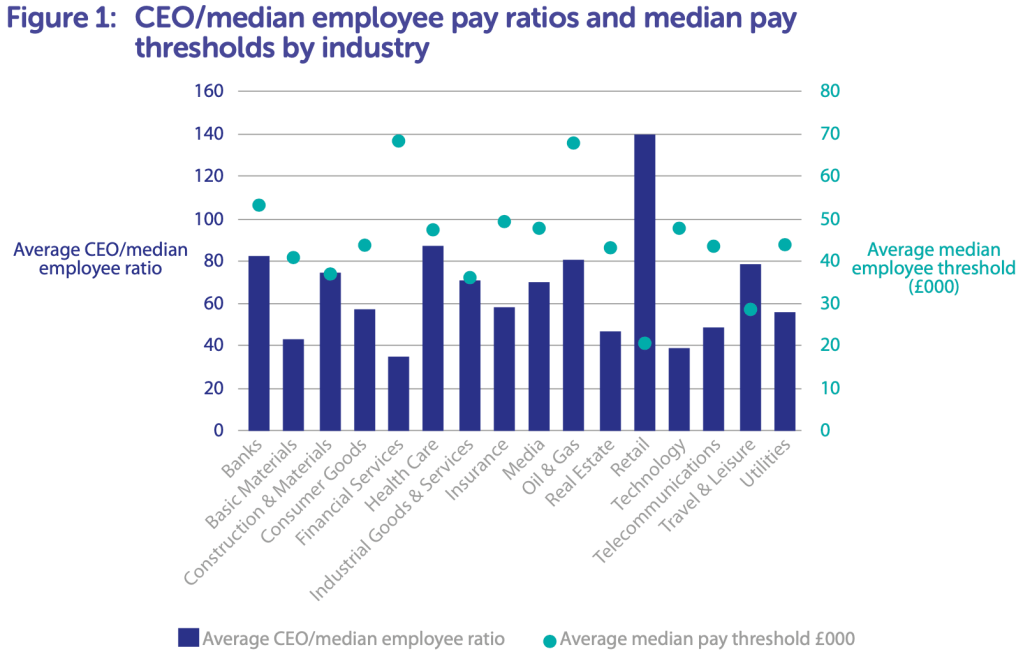

These averages mask some remarkable variation, with the highest ratio, 2605:1, being that at Ocado, whose Tim Steiner enjoyed (and one assumes continues to enjoy) an extraordinary one-off level of pay of £58 million. Another seven companies saw CEO:median paid employee ratios over 200:1 (JD Sports, Tesco, Watches of Switzerland, GVC Holdings, Morrisons, CRH and WH Smith). The variation is shown a little in this chart:

It is clear from this that the biggest driver of the largest ratios is less the CEO’s individual pay (setting aside the unusual case of Mr Steiner) and more the pay of the workforce. That is still starker when the ratios in comparison with lower quartile workers by pay are considered. At Ocado, this ratio is 2820:1, at BP it is 543:1 and at Tesco it is 355:1. There are some sectors that are disproportionately represented among those with high ratios and notably low levels of pay — particularly retail and hospitality [Note that while AB Foods is classified as a ‘consumer goods’ company, its lower quartile paid workers are likely to be employed at its Primark subsidiary]:

In 11 cases, the High Pay Centre notes, the revealed lower quartile thresholds are below what would be earned from a 35-hour week paid at the £9.30 real living wage as calculated by the Living Wage Foundation (note, this is not the statutory minimum wage – no allegation of illegality is being made). We should note that in part these sectors being notably lower paid is an output of long-standing sexism in pay: retail and hospitality have traditionally been seen predominantly as women’s work and so have never been paid as well as other sectors. That is a clear unfairness.

And it is important to note that, as low as the pay revealed by these lower quartile figures is, fully a quarter of the workforces of each company is paid less.

When we focus on the lowest paid, it’s important to note as the High Pay Centre does that this data includes only those people that companies actually employ. HPC argues that outsourced workers should be included in pay ratios; I’m not convinced that this is practical, but I think it is realistic to ask for greater clarity of disclosure in business model reporting of all the additional workforce on which the company is dependent that are not necessarily staff members. More general enhancements to workforce discussions in business model reporting would also be helpful because these pay ratio disclosures include only UK workers. For some companies that will cover the whole business, while for others it is only a very small portion. Business model reporting can be made much more transparent and informative, and these sorts of disclosures would help towards a better understanding of how each company sits within its broader economic environment.

The High Pay Centre also calls for a number of ways in which the accountability of companies, and particularly remuneration committees, for pay decisions — including outcomes like pay ratios — should be enhanced. Personally, I have long said that there should be greater formal accountability of remuneration committees to staff members, in particular a formal presentation annually by the remuneration chair to employee representatives. I think that could prove salutary, and be a strong route for understanding staff perspectives that could then be fed into discussions in the boardroom. It might also help alleviate some of the ongoing suspicions that CEOs and other executives have too much influence on their own pay.

CEOs may be tempted to leave their decorations up. I suspect the rest of us will be moved to take ours down.

See also: Resentment and rents: fairness in executive pay

High Pay Day 2021, High Pay Centre

Pay Ratios and the FTSE 350: An analysis of the first disclosures, High Pay Centre, December 2020