“I understand and appreciate the British sense of fairness and I do not wish my tax status to be a distraction for my husband or to affect my family.”

It is welcome to hear anyone refer to the sense of fairness. But when that woman is a millionaire who happens to be married to a cabinet minister, the reference perhaps gains an added resonance. It’s a shame though, when it appears that the sense of fairness is only brought to bear to drive a change in behaviour following newspaper headlines, and both personal and political embarrassment.

I don’t wish to linger particularly over the personal choices of Akshata Murty, daughter of the founder of India’s tech giant Infosys and wife of British Chancellor of the Exchequer Rishi Sunak, to start paying UK tax on her worldwide income rather than just that remitted to the UK – though notably she is choosing to retain her non-domiciled status for inheritance tax purposes, likely to be a much more valuable decision. And I’m sure that I should at this stage note more generally that I make no comment on the tax position of Murty, or any other individual or corporation. Her comments serve simply as an introduction to general thoughts that are not intended to have any particular target.

Tax is, famously, one of only two certainties in life. For most of us, it is indeed a fixed certainty. Yet as Murty shows, for the wealthy – and for companies – tax is rather more a matter of choice. We need to assume that no one evades taxes (that is, after all, illegal – though this story from the FT just today suggests that we and the tax authorities simply don’t know) but by linguistic sleight of hand and legalistic structuring, some do avoid it.

Tax expert Dan Neidle, newly retired from Clifford Chance and now operating as Tax Policy Associates, explains several of the choices that are available to the wealthy to limit their tax bills – see for example his briskly entertaining ‘How to avoid UK tax if you’re an oligarch’. The wealthy can choose to take income in forms that aren’t income for tax purposes, or which are taxed at a lower threshold. They can decide to take the benefit of capital gains without ever crystallising them, they can use trusts and corporate structures to pass ownership through the generations without facing inheritance taxes.

Multinational companies have even more choices of ways to smooth their tax burdens and avoid (never evade) taxes. Just as ordinary folk don’t have the options that are available to the wealthy, domestic companies face many more constraints and have fewer choices available to them. This can mean that multinationals are handed a further advantage and can undercut their more heavily taxed local rivals.

There are of course multiple attempts by the tax authorities to limit the choices available to those who have them. The G7 tax deal from this time last year attempts to set a minimum tax level of 15% globally (though with many exceptions and caveats that reduce its effectiveness). In a similar way, individual countries, notably the US, set minimum tax levels for income taxes in an attempt to ensure individuals cannot use exemptions to bring their tax burden too far below the nation’s headline rate. It should be said, though, that the US’s Alternative Minimum Tax (of 26% or 28%) itself has several degrees of complexity, and as I have noted, the wealthy need not take all of their income (as broadly understood) as income in the narrower way that tax regimes understand it. Given that income levels can be so manipulated, it is not surprising that there are increasing calls for taxes based on wealth rather than on income.

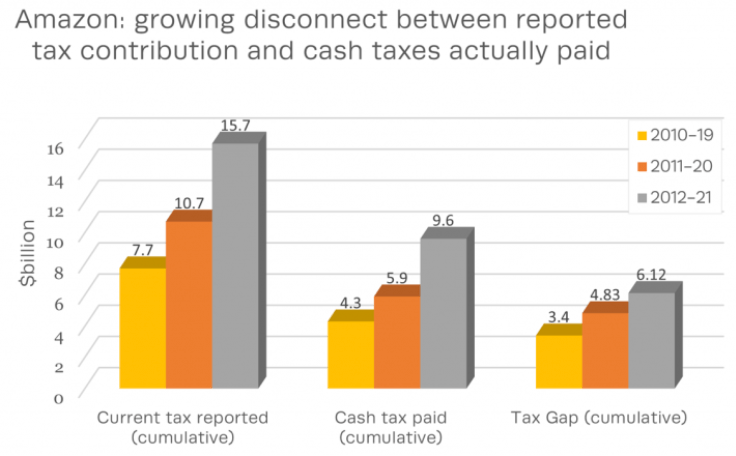

The way the choices that companies make can play out is amply demonstrated by the ongoing work by the Fair Tax Foundation (now preparing for the rapidly-approaching 2022 Fair Tax Week) in looking at the tax gaps of the so-called Silicon Six – Alphabet (Google), Amazon, Apple, Meta (Facebook), Microsoft and Netflix. The tax gap is the often large gap between cash tax paid and that provided for in accounts. The Foundation’s recent update on Amazon shows that its tax gap continues to grow:

Amazon faced a shareholder proposal at its AGM this week, calling for the company to issue a tax transparency report. In its formal response to this proposal, the board did not argue against tax transparency, but did note that “we believe the prescriptive granularity of the GRI Tax Standard’s reporting would potentially force disclosure of competitively sensitive information about our operations and cost structures and would hamper our ability to make operational decisions”. It also suggested that the focus on income taxes is mistaken and that its property and payroll taxes (both of which are much harder to avoid) should also be taken into account.

Perhaps Amazon should take care with this argument: just as with individuals, if income taxation falls into disrepute it may be that there is a shift to other ways to calculate tax liabilities for companies, in ways that may be less easy to avoid. In any case, independent shareholders did not seem particularly persuaded by the company’s arguments, with around 21% of them voting for the proposal. This provides a sign that shareholders are more willing to press for tax transparency.

Let’s hope so. Investors need to have more conversations with companies about tax matters. In my experience, it was only the language of fairness that elicited useful discussions on tax with company boards. Companies have had detailed advice on their structures and – except in the most unusual circumstances – what they do is legal. But they need to consider whether the choices that they make are fair and just. My best conversations with board chairs always focused on whether there was some tax structure or approach that might cause the company embarrassment. The scale of tax gaps can be a sign that there is an issue, essentially where there is a sizeable gap between cash tax paid and the headline rate of the home jurisdiction. Where such a gap is big, there’s a danger that a fair approach has not been applied – and that profit margins may not be sustainable in the long-run as the tax rate actually paid becomes fairer. That is certainly something that should matter to all investors.

Tax should be a certainty. Tax is the entry fee to a civilised society, and while the wealthy may feel that they can pay privately for everything that society provides they are more dependent than they wish to admit. They may tend to take for granted the availability of staff and the general good running of the state, but these are things that all of us depend upon and which themselves depend upon a functional society that is able to fund itself, in part at least, through taxation. States need to be able reliably to raise the funds that they need, confident that the tax levied will be paid as due. Tax should be a certainty, not a choice.

For those who have such choices, I would naturally agree that the sense of fairness should be the main driver of deciding what are the appropriate choices they should make. But tax shouldn’t be a choice. Like death, it should be a certainty for us all. If the rules aren’t yet smart enough to make that so, then it is only fair that they should be toughened up.

See also: The maybe fair tax deal

Akshata Murty Twitter thread April 9 2022 @anmurty

UK admits it has no idea how much tax is being evaded through offshore assets, Emma Agyemang, Financial Times, May 29 2022

How to avoid UK tax if you’re an oligarch, Dan Neidle, Tax Policy Associates, May 8 2022

Amazon’s tax gap grows to more than $6 billion as progressive investors push for transparency at their AGM, Fair Tax Foundation, May 23 2022

Fair Tax Week 2022, June 11-19