A version of my brief comments at the launch event for the latest High Pay Centre analysis of FTSE 350 pay ratios

This refreshed analysis is highly welcome and timely. We should remind selves that this is a political disclosure. For example, the fact that the disclosure is regarding the UK workforce means that its information value is purely local, and not about the businesses as a whole. Its information value for investors is limited because of that – and I’ll discuss ways of giving investors more insight into low pay issues – but its value as a political tool is clear.

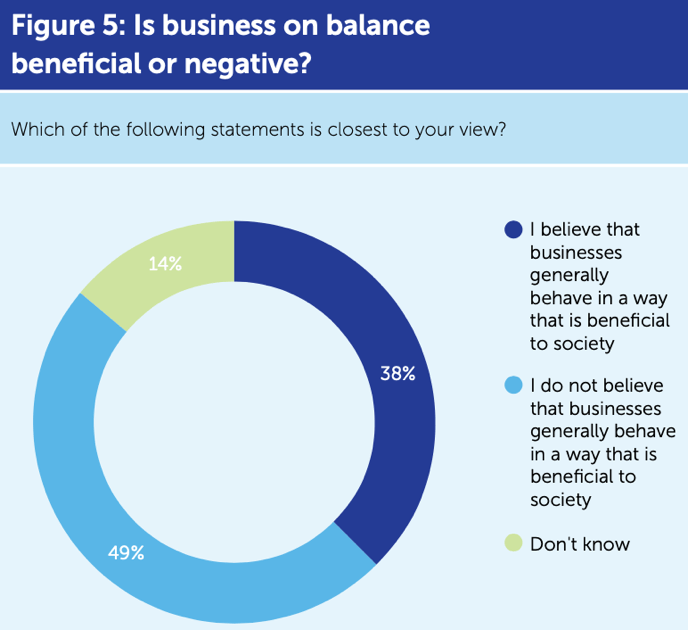

Political disclosure and the politics matters. It’s a real problem for all in business that there’s an 11% deficit on the public’s view of whether business operates in a way that’s beneficial for society. This key outcome from the High Pay Centre’s public opinion survey carried out by Survation, showing fully 49% of people do not believe that businesses generally behave in a way that is beneficial to society, is a problem for all those interested in business, including all investors. That this is the balance of public opinion at the start of a cost of living crisis is actually potentially dangerous – one assumes that as life gets harder for so many of us, so opinions will harden in an unfavourable and increasingly problematic way.

That could be politically difficult. Unfairness fosters all sorts of problems, political and societal.

To use the political power of public naming, as last year, I think it is appropriate specifically to call out those companies that have not disclosed the pay data on their workforces as they should. According to the report, this year there are fewer than last year’s 11, but seven companies continue not to disclose what they should. Centrica, Electrocomponents, Ibstock, Pearson, Pets at Home, Rentokil and JD Wetherspoon could all do better.

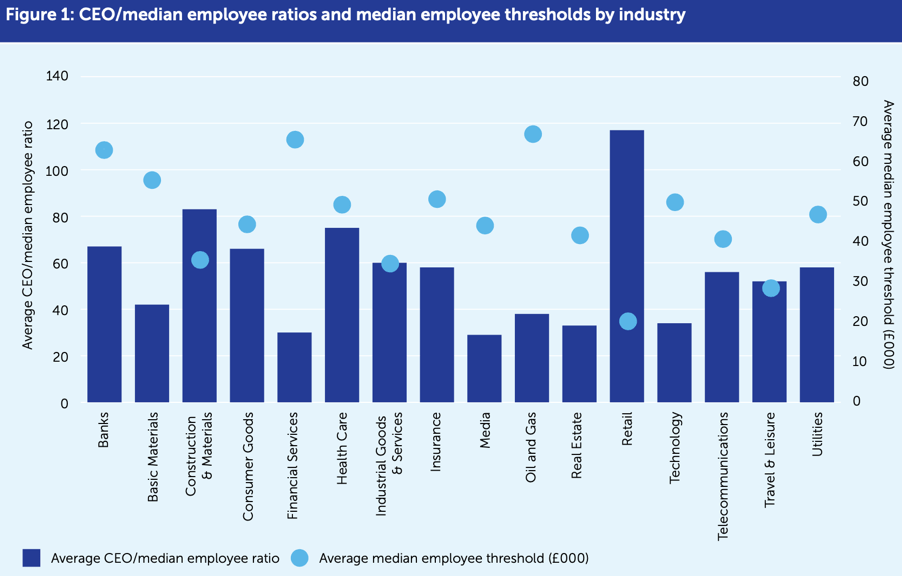

It is clear again from the data that the biggest driver of these high pay ratios is low pay among the workforce, not so much high pay of the CEOs. The chart below comparing industries makes this plain, with the highest pay ratios coinciding generally with the lowest median pay among the workforce (it would be clearer if the scale for the pay levels was inverted, but the correlation is pretty clear anyway). Looked at in this way, there are some clear outliers – notably that even though median pay in the banking sector is high, the ratio is also high, contrasting with financial services more broadly (median pay appears similar at around £65,000, but ratio at financial services is about half that of banks, about 30:1 rather than over 60:1). At other end of the spectrum, it seems clear that the main driver of the high pay ratios in retail appears to be low pay. Yet the next worst-paying sector travel and leisure (which reports median pay maybe 50% higher but still under £30,000) has pay ratios under half the level of the retail sector. There’s a correlation but there are nevertheless clear variations in the approaches of different sectors.

As the biggest driver of these issues is low pay, we need greater disclosure of pay structures and approaches at this end of the pay spectrum. This would allow investors and other stakeholders to understand business models more clearly. As inflation adds pressure to increase pay, understanding these dynamics will gain added importance. In a previous blog, I’ve argued that companies should be required to disclose: (1) the number of full-time equivalent roles in their business and (2) the proportion of those roles that pay a living wage. I don’t diminish the challenge of calculating the latter for many countries, but there’s a lot of work gone into it so it is possible. Actually seeing which companies pay their people enough to live on and to bring up a family with dignity is surely a key metric. These two measures are also aggregable so can be considered across portfolios, something which matters to investment institutions, particularly asset owners. [This recommendation was kindly – and nearly accurately – picked up by Nils Pratley in The Guardian; “Good idea: a league table would get noticed and may cause more embarrassment,” he says].

A further way that the disclosures on low pay are deficient is, as the report notes, the exclusion of many of the lowest paid from the calculations. The exclusion of agency staff, including temps and cleaners and so on, clearly diminishes the insights the reporting gives, both for investors and for political purposes. Finding ways to capture the workforce more generally would be helpful.

The question of inflationary pressures on wages will be a key one for the next few years. It’s worth noting that inflation is experienced very differently at different income levels. Different groups buy different baskets of goods, meaning that 9/10% headline inflation is not what any one group actually experiences. Analysis by the New Economics Foundation suggests that the variation could be as much as between 20% for the poorest and perhaps 2% for the richest; one hopes that remuneration committees bear this in mind when considering both the pay of top executives – who are unlikely to need anything close to headline inflation-level pay increases to maintain their standards of living – and the pay of the general workforce – who may need pay increases well above headline inflation to maintain theirs.

The pay ratio is a political metric, but that doesn’t mean investors and companies can ignore it. On the contrary, the current political and economic environment requires that they respond actively to this agenda. It is not in any of our interests that more people doubt the benefits of business for society than think it is a positive – and that that is true at the start of the cost of living crisis is genuinely a dangerous position for us.

We all need to pay more attention, and simply, to pay more.

High Pay Centre analysis of FTSE 350 pay ratios, High Pay Centre, May 2022

Launch event, May 23 2022

THG boss should count the blessings of life as a listed company, Nils Pratley, The Guardian, May 23 2022

Losing the inflation race, New Economics Foundation, May 5 2022