“low-paid workers continue to face a greater risk of receiving a pension that delivers an inadequate standard of living in retirement”

It’s the starkest of the conclusions of a new analysis of pension saving. This Resolution Foundation work reveals we are a long way away from having fair pensions.

If you talk to pensions specialists about making pensions fairer they tend to think immediately of GMP Equalisation – the arcane process of addressing historic gender inequalities in pensions. Though the issue has been known for some years, the complexities of addressing it mean it is far from finished working through the system. But huge though this unfairness is, there is a much greater issue out there: whether future pensions will be enough to avoid significant proportions of the population retiring into poverty. People may be being fooled into the current minimum savings requirements into thinking they will achieve the fair and comfortable retirement that people expect at the end of their working lives.

Unfortunately, the Resolution Foundation analysis on Living Pensions suggests that many will instead retire into destitution. The Living Pensions work is so-called because of its association with the Living Wage Foundation, which presses that pay should at least reach a minimum threshold that enables people to live a decent life. By analogy, the Living Pensions analysis seeks to identify levels of pension saving that should enable people to live a decent life in retirement – and it identifies how far away saving levels are currently from those needed to deliver that fair outcome.

The work on the Living Pension is based on the new world of pensions. I explain this new world briefly at the foot of this blog to avoid the details getting in the way of the message about fair pensions, and our current lack of them.

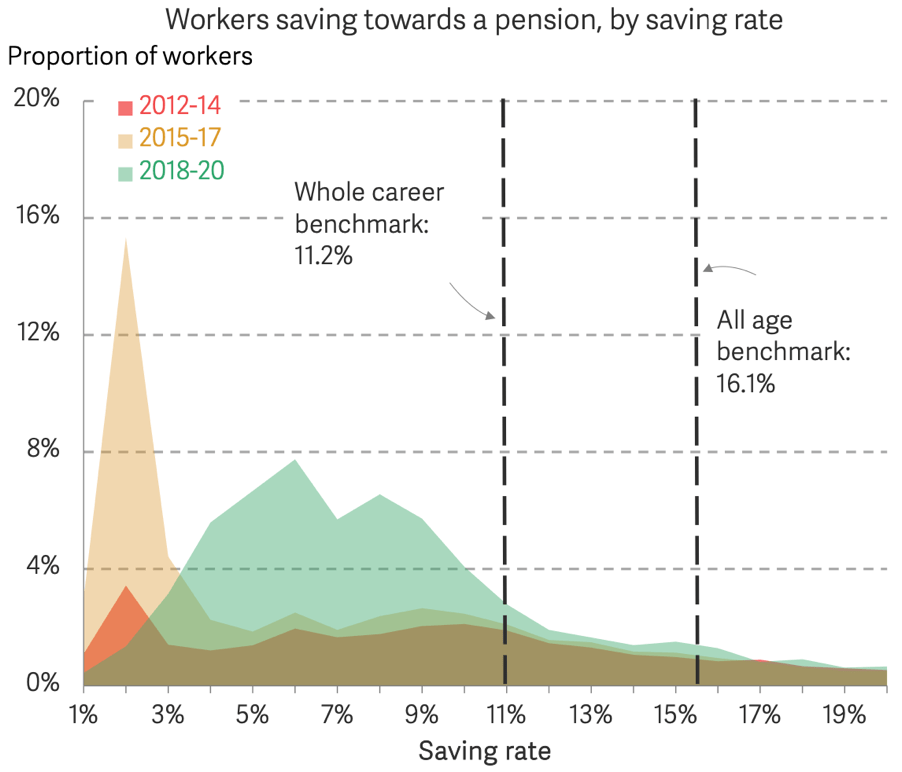

The Resolution Foundation’s work identifies minimum necessary savings levels of 11.2% for those saving for their whole working lives, or 16.1% for those starting to save later (in effect, some time in an individual’s 30s). In 2019, the minimum contribution level as a portion of salary that must be paid under auto-enrolment rose to 8%. Even though this 8% falls below the levels estimated necessary to achieve a Living Pension – it is notably half the rate estimated to be required for those who do not save for the whole of their working lives – it isn’t being achieved. “Given the influence the auto-enrolment scheme is having on workers’ contribution rates, it is not surprising that we find relatively few workers are saving at or above the [Living Pension] benchmarks,” says the Resolution Foundation. Statistics suggest saving levels for the poorest – where a fair pension threshold must matter most – may be as low as 3-5% on average.

Even with auto-enrolment, the Resolution Foundation analysis of ONS data shows that fully 35% of workers are still not saving into a pension at all. That number rises to 74% for those in the lowest fifth of earners – nearly half of whom do not earn enough to reach the threshold at which they must be auto-enrolled (£10,000; and contributions are only made on earnings above £6,240).

And that is before the cost of living crisis fully kicks in and makes more people study carefully every item of their expenditure, which may include paying into pensions. While every employee must be auto-enrolled into a DC scheme, everyone can choose to opt out and stop their contributions. Anecdotes suggest an increase in opting out has already begun.

The overall statistics show, positively, an increase in overall levels of pension saving (though this is before any impact from the cost of living crisis). But they also show just how far below the necessary levels of saving we are overall:

No wonder that a number of pensions experts are very worried. Particularly striking was a recent LinkedIn post from Charlotte O’Leary, CEO of Pensions for Purpose, which began “I cried yesterday…”. Charlotte wonders if it will take a generation retiring into poverty before we as a nation begin to save more appropriately for our pensions.

Helpfully, the Living Pension calculations are not just based on percentages of salary but also offer absolute rates of saving necessary to build funds sufficient for a decent living standard in retirement. These are £2,100 a year for those saving for their whole working lives, and £3,000 for those who only start to save later. This has to make sense, and fits with the heritage of the Living Wage Foundation. Only real levels of cash can be lived off, not percentages of variable salaries over a working life. A Living Pension is only fair and can only amount to that baseline necessity if it provides an absolute threshold of cash that will keep people at a decent level of living.

Unfortunately, under 20% of us are reaching these thresholds for saving. The Resolution Foundation says: “82 per cent of workers (again, approximately 16 million) [in] 2018-20 were saving at or below the ‘whole career’ cash benchmark, and even more (89 per cent, or 18 million) were saving below the ‘all age’ cash benchmark.” Most of those saving at these levels are earning significantly more than the real living wage – almost all are in the top two-fifths of earners – so even those who are meeting the Living Pension cash thresholds risk finding their spending ability in retirement being much more constrained than they are used to. As with previous failures to deliver pension fairness, there is also a major gap between the sexes: 23% of men meet the ‘whole career’ cash benchmark, while only 15% of women do. We are storing up real problems for fairness in the future.

This point that calculating pensions merely as a percentage of salary may give the wrong answers and that we need to consider much more actively absolute numbers has a counterpoint at the upper end of the pay scale. Investors have pressed hard that executive directors should not receive pension benefits that go beyond those of the wider workforce – and now, some four years on from this being specifically referenced in the UK Corporate Governance Code and in investor expectations, this has largely been delivered (in the UK at least; elsewhere is another story) – at least in terms of the percentage of salary. But any fair assessment of whether the pension benefits go beyond those enjoyed by the broader workforce surely needs to go beyond just percentages: if percentages don’t tell the whole story regarding fair pensions at the bottom end of the pay scale, then perhaps we shouldn’t be so satisfied just with aligning percentages at the top end. Any company that is aspiring to be a fair wage employer needs also to consider being a fair pension one too, and that probably requires considerations of minimum cash payments into staff pension pots, not just percentage payments that may or may not match those enjoyed by the boss.

There is also a structural complexity to delivering fair pensions. My old pal and former colleague David Pitt-Watson made the point in questions at the launch event that the Living Pensions calculations entirely miss longevity risk – the pensions jargon for those who live longer than expected. Living longer is obviously a wonderful thing for the individual and their families in general terms – except that if their pension is based on a fixed pot of money, living longer risks individuals falling into destitution. Because they are based on average necessary pension pots, and based on a regulatory system that means every individual’s pension pot belongs to them alone, some of those with Living Pension average pots will die prior to their pension pot being used up and some will die after. Those who live longer risk having used up their pension pot before death and so having years where their pension isn’t fair, even if they have in fact reached the Living Pension threshold. The Living Pension in the context of the current defined contribution (DC) model may not turn out to deliver on the name even for half of those who achieve the threshold savings levels and fund value.

David has a long heritage in the world of pensions, and has helped lead work, not least at the RSA, on a new form of pension for the UK, Collective Defined Contribution (CDC). CDC pensions have just been given initial regulatory approval and we are likely to see the first launched shortly. CDC offers some opportunity to address this problem with the defined contribution world. The collective element of CDC allows pooling of longevity risk; it is only with such pooling that the unfairness of pots running out before an individual dies can be addressed.

In a personal conversation, David summarises the position simply: “It isn’t a pension if it’s just a cheque.” The work by industry body the Pensions and Lifetime Savings Association on its Retirement Living Standards re-emphasises this: its work on living standards in retirement is all about income not pension pots, and suggests a ‘minimum’ income in retirement needs to be £10,900, or £16,700 for a couple.

It seems that in a post-defined benefit world only within the context of CDC can fair pensions actually deliver on the promise of a Living Pension.

In brief: the new world of pensions

There are three aspects to the new world of pensions: the move from the historic Defined Benefit (DB) structure to a Defined Contribution (DC) approach; pension freedoms; and the requirement that all employers now offer all staff a workplace pension, through so-called auto-enrolment.

Defined Benefit pensions – sometimes called final salary schemes – were the promise from an employer that they would pay a fixed annual pension to former employees, based on their years of service and usually the final salary that they were paid. For example, many individuals built up promises worth a sixtieth of their salary for each year of service (though some schemes were based on fortieths or eightieths) – the benefit was the fixed element and employers promised to provide the funding necessary to support this. DB now feels like ancient history, partly because its implicit assumption of working for one employer for much of one’s career now seems an anachronism and partly because people lived a lot longer than expected, making the pensions promise much more expensive than planned. Companies have regretted their generosity and the balance sheet risks that such pensions brought and have largely withdrawn from offering defined benefits – though many are still funding those past promises. In large part, DB pensions are now only available in the public sector.

In the DC world the only thing that is fixed is, as the name suggests, the contribution – the amount of money put aside each month. This is used to buy investment products that hopefully will perform well enough to provide scope for pension payments after retirement. Individuals face much more risk in the DC world, especially investment risk over their lifetime of saving. While death, like taxes, is a certainty, its timing isn’t, and individuals in a DC world also take on the financial risk that a long life may bring, that even the largest pension pot may run out, with no sharing of risks and no backstop (other than state pension provisions).

Former chancellor George Osborne took the further step along this line of seeing pension saving just as the creation of a pot of money rather than a later-life income stream. In 2015 he announced what were billed as pensions freedoms – releasing the obligation to use pension pots to buy annuities (rights to income payments) and allowing people to unlock their pension pots for other purposes at the age of 55. Many have used this freedom wisely, but many have found it is a freedom to lose money through mistaken investments and fraud. Often it seems the wealthy have paid for valuable advice and the less well-off have been exploited by fraudsters. The full consequences of these freedoms are yet to be seen.

Automatic (usually auto-) enrolment is the requirement since 2012 that every employer should offer all staff paid more than a minimal level some form of pension provision. Minimum levels of saving are 8% of qualifying earnings (between £6,240 and £50,270), at least 3% from the employer and the remainder, up to 5%, from the employee (when first introduced the total auto-enrolment minimum was 2%, 1% from each party). This has helped drive much broader pension saving, and led to the creation of a number of specialist workplace pension providers, such as Nest and NOW Pensions. Nest in particular, the largest of the new providers, is now a substantial financial institution with £24 billion assets under management.

Full disclosure: I am a Nest customer and have provided some stewardship advice to NOW. I have also provided advice to a trustee of the likely first CDC pension provider.

Living Pensions: An assessment of whether workers’ pension saving meets a ‘living pension’ benchmark, Nye Cominetti, Felicia Odamtten, Resolution Foundation, July 2022

“I cried yesterday…”, Charlotte O’Leary, CEO, Pensions for Purpose, LinkedIn post, 3 August 2022

UK Corporate Governance Code 2018, Financial Reporting Council

Investors to Target Pension Perks and Poor Diversity in 2019 AGM Season, the Investment Association, 21 February 2019

On track for fair pensions launch event, 28 July 2022

Collective Defined Contribution Pensions Forum, RSA

A new third way for pension savers, Guy Opperman, Pensions Age, 1 August 2022

Retirement Living Standards, Pensions and Lifetime Savings Association

Should people be saving more for retirement?, Institute for Fiscal Studies podcast, 10 February 2022