It seems certain that taxes will have to rise, at least in due course. It will not be the full answer to this need, but fairness demands that a simple first step must be to close loopholes and deal with anomalies in the system. I’ll write shortly again about corporate taxation, but this blog is regarding the unfairness embodied in capital gains taxation.

Just as anomalies around differential taxation of the self-employed have been exposed by Covid bail-outs applying in an equivalent way to them as to furloughed employees, so have the anomalies around personal service companies. These are used by individuals to offer out their consulting and advisory services, paying out income as dividends and used as stores of value that can be unlocked as capital gains at winding up — both forms of income facing lower levels of taxation than employee rates. Again, many of these individuals have sought Covid bail outs as if they were employees. The bail-outs imply that we are all in this together, but the prior tax advantages of this small group indicate again that we most definitely are not.

To give some shape to the disparity of the distribution of taxable gains, the US’s Tax Policy Center identifies that the top 1% of taxpayers by income received around 75% of the total benefit from that country’s preferential tax treatment of capital gains. This is far from fair and equal:

“Preferences for capital gain and dividend income will reduce tax burdens in 2019 by 5.7 percent of income in the top 1 percent of the income distribution, compared with 1.4 percent of income for other taxpayers in the top 5 percent of the income distribution and a smaller share of income for lower-income groups.”

Few taxes are as regressive in their impacts. The unfairness could be removed by equalising the tax rates charged.

The UK and much of the wider world, including the US (at least for gains on assets held for more than 1 year), charge lower tax rates on capital gains than on income. Personal service companies are just one way in which this differential is exploited by those able to choose to take income as gains. Another is carried interest, through which a number of private equity and other investment professionals are paid significant portions of their reward — in a form that is ostensibly aligned with the interests of their clients.

The Resolution Foundation recently issued a report highlighting the extent of capital gains as a portion of the overall level of income in the economy. Using HMRC data analysed by a team based at LSE, the paper identifies the significance of taxable capital gains, worth some £55 billion overall in 2017-8. While this represents around £1000 for every adult in the UK, it is much more highly concentrated even than overall income levels: that total was shared by only 260,000 individuals and 62% of it was received by just 9000 individuals, each of whom gained more than £1 million.

The fact that much of this is income by another name is amply demonstrated by a chart that does not seem to appear in the report but was part of the associated presentation. This shows the persistence of taxable capital gains: fully a third of those with significant taxable gains in one year had also had significant gains in recent prior years. Gains are less lumpy than theory would indicate, suggestive of this being an exploited loophole.

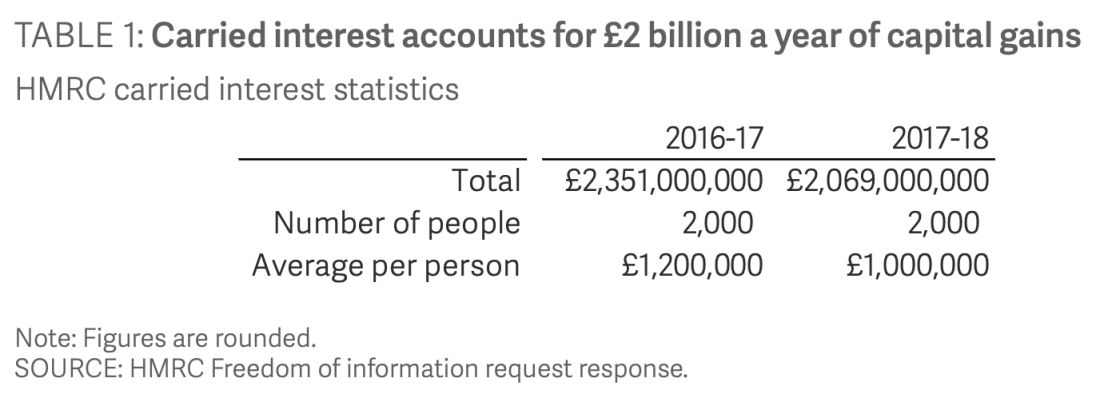

One of those areas likely to be persistent, because it clearly is income in another form, is carried interest. This is a very significant income for a small handful of individuals, as the table of data gleaned from HMRC under FOI legislation amply shows:

Those benefiting from the favourable treatment of capital gains are already well paid: 45% of all gains were received by those in the top 1% of income earners (understanding income now in the narrow sense usually used, ie excluding gains). Only a tenth of the top 1% of income earners change when capital gains are included in the calculation. And the existence of capital gains makes the disparity between the haves and have nots starker than it is already: the top 1% by income take home fully 13.8% of overall income; when gains are included, the top 1% receive 16.8% of the total pie. Including capital gains in income calculations for other countries also leads to greater apparent disparities, and disparities that are also increasing over time. We know that capital has been favoured over employment since the financial crisis, and this is the natural — and unfair — consequence.

It is clear that the favourable tax treatment of capital gains is unfair, and in the context of a need for taxes overall to rise, it is also unsustainable.

But perhaps we should not stop there: taxable capital gains are an understatement of overall capital gains enjoyed by recipients. Loopholes could also be closed. For example in the UK there is an annual capital gains allowance, currently £12,300, meaning gains less than this are not taxed at all. Removing this allowance, perhaps just for those calculating self-assessment tax (ie all higher earners), would seem fairer. Cars are exempt, which is bizarre given that it can only be a very small subset of cars that ever see a gain in valuation — a subset open only to the wealthiest owners. Gifts to spouses and civil partners are exempt also, allowing some sharing out of assets (at the same time sharing capital gains, and indeed inheritance tax, allowances). Removing these exemptions seems logical and fair. More justifiable economically is the exemption for the gains on a main residence given that taxation of those might potentially have a chilling effect on mobility and freeing up unused property.

Capital gains taxation is only one example of income from wealth being taxed less heavily than income from work. That differential tax burden seems unfair and unjustifiable, and now is probably the time for that broader unfairness to be addressed also. One step in the right direction might be a land value tax. In an environment that will need economic stimulus, such a tax could have the benefit of promoting economic activity by giving an incentive to put assets to good use. The taxation of unearned gains, such as those from winning the lottery of planning consent, might need to be more generally considered. Whether we are ready yet for broader wealth taxation may be doubtful, but taxation focused on land, and on gains on land values, do have the benefit that these cannot be expatriated and taken beyond the reach of the exchequer.

Radical steps have already been taken to keep the economy alive. Radical steps will be needed to rebuild the fiscal base. Fairness needs to be part of those considerations.

The LSE team are holding a forthcoming webinar on their tax research:

How Much Tax Do The Rich Really Pay And Could They Pay More?

Monday 15 June 2020 4:00pm to 5:30pm

Distributional Effects of Individual Income Tax Expenditures After the 2017 Tax Cuts and Jobs Act, Tax Policy Center, June 2019

Who gains? The importance of accounting for capital gains, Resolution Foundation, May 2020