Institutional investors wave through pay practices that are unfair — to themselves as well as to others. Even the best barely manage to arrive half-way towards fairness. Funds thus fail to have fairness at the heart of what they do.

These are the conclusions of a fascinating recent presentation by Steve O’Byrne and his Shareholder Value Advisors, still available as part of an on-demand webinar (at least at the time of writing).

It’s worth noting of course that Steve has developed a particular definition of fairness, and his own detailed statistical analysis of whether companies deliver it — and also whether investors respond appropriately. But the mere fact that he considers fairness is clearly welcome, and his analysis at the least confirms that there is a problem (as if further confirmation were needed). It’s worth also noting that he focuses purely on the US, where that problem is arguably greatest, and his main focus with regards to investors is their voting on so-called ‘say-on-pay’ resolutions, the normally annual non-binding votes to approve company pay practices.

Steve’s definition of unfairness is essentially one of excess rents — ie payouts that are undeserved, essentially because they provide rewards for performance that is no better than the industry standard. By this definition, these are unearned payments and so should not form part of any individual’s earnings. To the extent that investors are supporting payments that amount to unearned rents they are harming their own returns and signing off on skewed economics.

He has developed what he believes to be the perfect structure for a fair pay scheme, which derives awards based on TSR and the level of vesting based on returns greater than the industry. Whether everyone would deem the outcomes of these calculations ‘fair’ may be in some doubt, as the starting point is ‘market pay’, ie it assumes that generally pervading pay levels for top US executives are appropriate, in effect baking in current levels of unfairness. Nonetheless, the model does appear to deliver some greater relative fairness between executives and between companies, and it is a useful thought experiment stepping towards a broader fairness that reflects economic rationality. Steve is good enough to recognise that there is another form of ‘perfect’ pay structure to have been proposed for corporations: the Dynamic CEO Compensation model developed by excellent UK academic Alex Edmans. Both this, and Steve’s own version of perfection, have some striking similarities with the proposals for lifetime restricted stock compensation that a number of investors (notably Norges Bank and Hermes) have been trying to promote.

While there are dangers in a focus on TSR — this must always be an output of decision-making and there are dangers in bringing it into the foreground through making it a metric — over the long term it should be a reasonably fair measure. It is usually regarded by investors as the least gamable of performance measures. It is potentially subject to gaming, yes, but less so than other metrics and with fewer perverse incentives built into it.

In some ways, it appears that investors are doing a good job: Steve identifies a high correlation between votes against US say-on-pay resolutions and the amount by which CEO pay exceeds fair levels in terms of company size, industry and relative TSR. However, he notes “extraordinarily high pay premiums are needed to get a majority ‘no’ vote” so majority opposition is only brought about by truly egregious cases. His other yardsticks on fairness include whether the CEO is paid more than 2.5x the median of the other 4 disclosed highest earners at the company and assessing pay against relative returns on invested capital. Both seem sensible measures of some aspects of fairness, though it is impossible to know if the calibration set is the right one.

However, despite this limited positive, two of Steve’s overall conclusions are pretty damning:

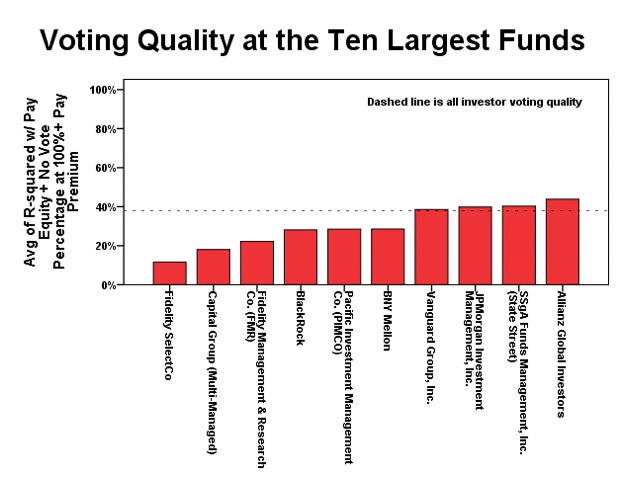

- only 3 of 213 funds are halfway to what he would say is fully informed and fair say-on-pay voting (kudos to Irish Life, Calvert and to Wells Fargo, which leads the pack with a calculated 56% vote quality); and

- three quarters of funds vote with a lower quality than the overall average, which itself is sadly below 40% of perfectly fair levels according to the calculations.

And his chart on the fair voting performance of the largest fund managers is unimpressive:

BlackRock is the only one of these for which he provides broken out data, and the 28% average according to Steve’s calculation is dragged down in particular by his analysis that the firm votes against only 7% of those situations where the CEO’s pay premium above a fair level is more than 100%.

It must be clear that this is an idiosyncratic analysis, and a particular and personal perspective on fairness. No doubt through other lenses the performance of the investment industry would appear better. But the clients of the industry, who can only dream of the rewards received by top CEOs — and would welcome small portions of the pay inflation that they have enjoyed — could certainly be forgiven for asking if this is fair. It is further evidence that too many investors continue to be content to allow the persistence of much unfairness, in effect facilitating it.

One thought on “Funds facilitate unfair pay”

Comments are closed.